Roku — Q1 2021

A quick breakdown and update of Roku's most recent financial statements, stock price, valuation, and short interest.

Roku was blistering hot in 2020, fueled by the Covid-19 pandemic. Interestingly, Roku doesn't seem to be cooling off anytime soon — in fact, they may just be getting started.

Roku tends to be a very misunderstood business. People lean into the idea that Roku is just another streaming service in a world that is overflowing with subscription streaming content, though this is not at all the case. Roku, at their core, is a software company that empowers TV manufacturers across the globe with their proprietary operating system. These TV manufacturer partnerships coupled with Roku's own set-top streaming boxes makes Roku OS widely acceptable for all levels of consumers, bring Roku's user-base to new all-time highs each quarter.

But enough about Roku as a business, let's jump into the reason you're here: to look inside Roku's financials.

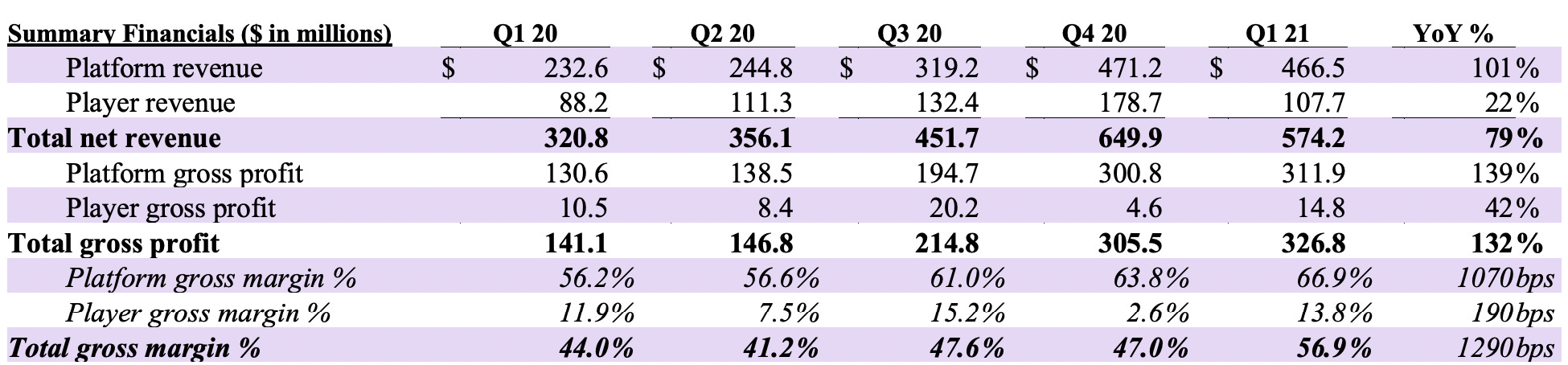

Roku totaled a net revenue of $1.78B in 2020, split roughly 70/30 between their two "divisions" — Roku Platform and Roku Player. Roku Player (the hardware side of the business) brought in just $510M in revenue in 2020, or about 29% of Roku's total revenue, but still grew at 31.6% year-over-year. Likewise, Roku Platform (the software side) brought in the remaining $1.27B, a staggering 71.1% increase year-over-year.

This has all been predetermined by Roku as they knew eventually their software would bring in far more revenue than their hardware, it was only a matter of time; this is why Roku Player has such poor gross profit margins (around 13%) — Roku's main goal with their hardware is to get users onto their platform and using their software, which is where Roku truly excels. Roku Platform currently carries a whopping 66.9% gross profit margin and is growing quarter-over-quarter. Since Roku Platform is also bringing in majority of the revenue, we see Roku's total gross margin accelerating upward, positing an all-time high of 56.9% in Q1 2021 (up 1290bps year-over-year).

Of course, Roku is still a "growth" company, which is evident by their operating expenses. In 2020, Roku spent $828M in operating expenses — a 47.8% increase from the $560M they spent in 2019. Regardless of how it may seem, this is a good thing. Roku is betting on themselves and their future, and in a big way.

As you may have put together by this point, Roku still isn't profitable. That said, they have had three profitable quarters in a row, with the company posting their first ever profitable quarter during Q3 2020 — a huge milestone. Roku posted profits of $12M in Q3 2020, $65.2M in Q4 2020, and $75.8M in Q1 2021, so they've been on a nice little run here. While I wouldn't necessarily deem another unprofitable year from Roku out of the question, I would certainly place my chips on 2021 being Roku's first profitable year since its inception, and first of many to follow.

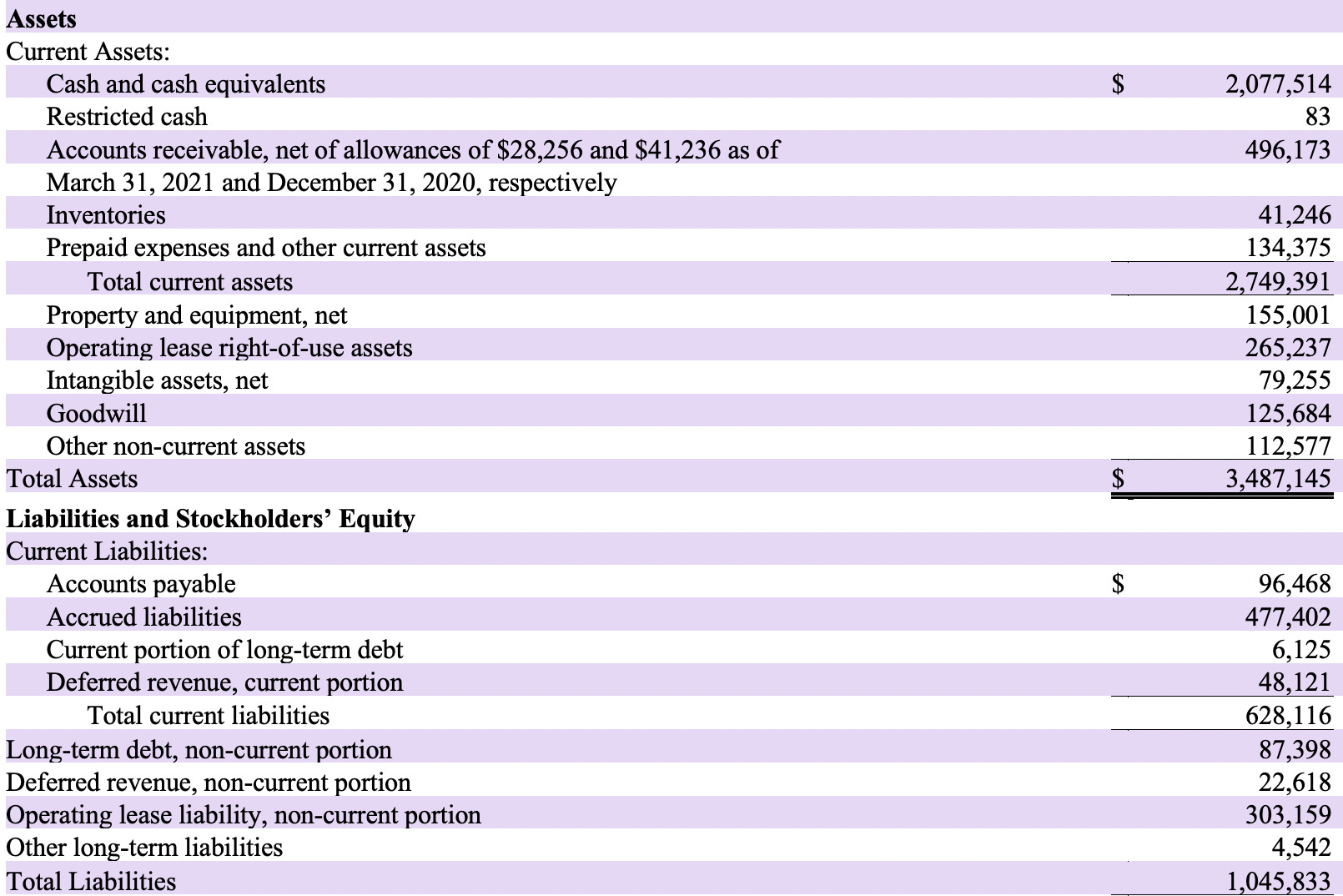

As of Q1 2021, Roku is currently sitting on:

$2.75B in current assets (over $1B more than they had the previous quarter)

$3.49B in total assets

$628M in current liabilities

$1.05B in total liabilities

Thus, Roku's total assets can pay off total liabilities 3x over, giving Roku ample room to continue expanding their offerings, creeping into international markets, and making critical acquisitions like dataxu and Nielsen's AVA business.

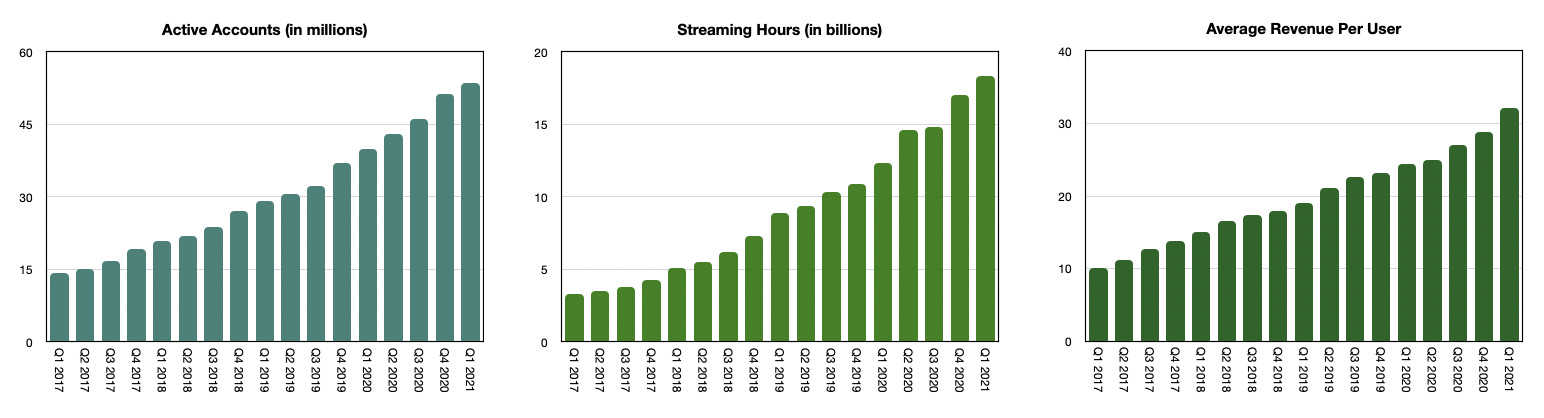

Now let's look at some of the defining numbers that don't show up on Roku's income statements and balance sheets.

Roku's active accounts, streaming hours, and average revenue per user (ARPU) haven't decreased quarter-over-quarter since becoming a public company. Read that again.

In Q1 2021, Roku's active accounts reached a new high of 56.3M — this comes after adding over 14M accounts in 2020 alone. They also announced that streaming hours totaled 18.3M for Q1 2021, a 49% increase year-over-year. Lastly, and perhaps most importantly, Roku's ARPU rose 32% year-over-year to $32.14 in Q1 2021, making them the industry leader in the category, beating Amazon's Fire TV and Google's Chromecast.

As you can see, Roku appears to be firing on all cylinders on this front. I'm excited to see what the future holds.

Lastly, let's quickly skim over Roku's stock price, valuation, and short interest (at the time of writing).

Roku currently trades at $399.99 and is up 160.90% over the past year, via Yahoo Finance.

Roku has a market cap of $53.75B with 132,399,000 shares outstanding, via Yahoo Finance.

3,790,000 shares are currently being shorted, giving Roku a short interest percentage of 2.86%, via MarketBeat.

Roku has a P/E of 470.58, a P/S of 25.40, and an EV/EBIDTA of 250.82, via Morningstar.

Roku has an institutional ownership of 70.74%, via Nasdaq.

Quickly, let’s compare Roku’s valuation metrics to some of its “growth” peers:

Square (NYSE: SQ) has a P/E of 312.53, a P/S of 8.99, and an EV/EBIDTA of 209.69.

Fiverr (NYSE: FVRR) has a P/E of 742.95, a P/S of 30.41, and their EV/EBIDTA is N/A.

Tesla (NASDAQ: TSLA) has a P/E of 637.84, a P/S of 20.04, and an EV/EBIDTA of 131.48.

Zoom (NASDAQ: ZM) has a P/E of 124.82, a P/S of 33.19, and an EV/EBIDTA of 113.79.

I’ll leave it up to you to decide where Roku’s current valuation stands amongst its peers.

And with that, this concludes out article.

If you enjoyed this issue of "Five Minute Financials" please consider subscribing for future financial breakdowns. If you want to learn more about Roku's business model, financials, management, competition, and potential, visit the “Business Breakdowns” newsletter on my Substack, or simply click here — you will be redirected to a lengthy deep-dive that I posted a while back, where I discuss all things Roku.

Thanks for reading! Be safe and take care.

— Nick