Shopify — Q2 2021

Shopify — Q2 2021

A quick breakdown and update of Shopify's most recent financial statements, stock price, valuation, and short interest.

Shopify tells two tales.

Some recognize Shopify as just “a website builder” — indifferent from Wix, Squarespace, or any other run-of-the-mill website-building platform. Others view it as the go-to-market eCommerce on-ramp that breaches the barriers, bridges the gaps, and fills the holes between concrete brick-and-mortar stores and beautiful, all-encompassing digital storefronts.

However you view Shopify, there is no denying it — this company has executed beyond wildest expectations.

Shopify has transformed from a snowboard shop to a comprehensive, data-stacked digital business enhancer, capable of helping their clients optimize every facet of their business, including:

online storefronts

multiple sales channels

advertising

shipping, labeling, and handling

warehousing and inventory

transactions and payment processing

point-of-sale systems

global selling

Needless to say, Shopify is ready and willing to fully transform any small business into a conglomerate, capable of powering every step of the process.

Shopify’s mission statement is:

To make commerce better for everyone, so businesses can focus on what they do best: building and selling their products.

As a bonus, Shopify is making everyone’s financial lives better throughout the process… well, at least everyone who has invested in them.

In this issue of “Five Minute Financials,” we will cover Shopify’s:

income statement

balance sheet

cash flow

operational metrics

stock price

valuation

Trust me, despite whatever perception of Shopify you may already have in your head, you will be firmly impressed with how monumental, stable, and superior this company is.

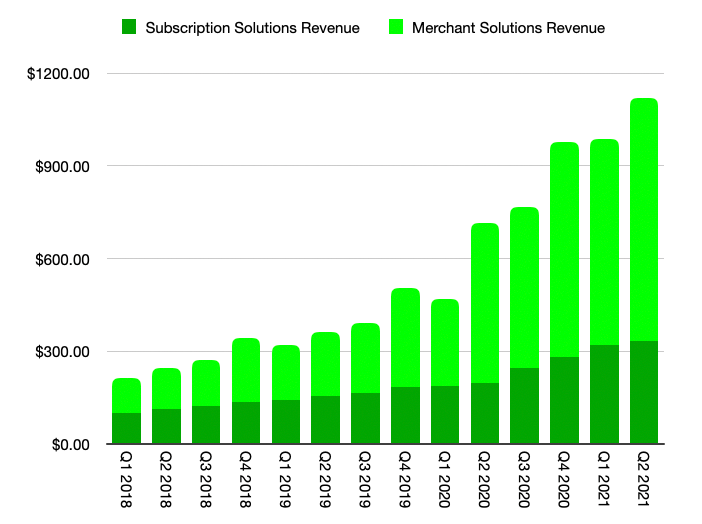

In 2020, Shopify reported full-year revenue of $2.93B, up a casual 86% from 2019. To back it up, the company went on to post outstanding numbers in Q1 and Q2 of 2021, coming in at $989M and $1.12B, respectively — this suggests that Shopify will do well over $4B in full-year revenue. By looking at the graphs below, you will be able to see just how incredible Shopify’s revenue growth has been over the past seven years.

To put it into perspective, Shopify did more in revenue in Q2 2021 than they did in the entire year in 2018 — that’s not even three full years ago.

Shopify’s revenue is split between two business segments:

Subscription Solutions

This revenue is from store subscription plans, which merchants must pay to use Shopify’s platform. Like pretty much everything nowadays, there are subscription tiers, ranging from $29 to $299 per month. There is also a newly added subscription tier, called Shopify Plus — this offers the best of everything that Shopify has to offer, plus more. It currently starts at $2,000 per month.

Merchant Solutions

This revenue is Shopify’s bread and butter, primed to completely dwarf their subscription revenue over time. Merchant revenue comes from payment processing fees, transaction fees, referral fees, and point-of-sale hardware sales.

In a way, Shopify’s business model is very similar to Roku’s — bring customers onto your platform for as little as possible, help them grow through proprietary advanced solutions, and profit immensely from this growth in a much higher-margin area of business. Brilliant.

Now that we have briefly touched on Shopify’s two main revenue streams, let’s see how they contribute to the whole puzzle.

I think we all see where this is headed.

Now, I know what you’re thinking, and I agree — Covid-19 undoubtedly streamlined Shopify’s revenue growth, propelling them to projections that were years away. I’m not one to argue. However, what matters most here is that their merchants aren’t leaving, thanks to the incredibly sticky, high-trust ecosystem that Shopify has built. Shopify’s recent influx of merchants might just be getting started — the company’s net merchant retention consistently hovers right around 100%.

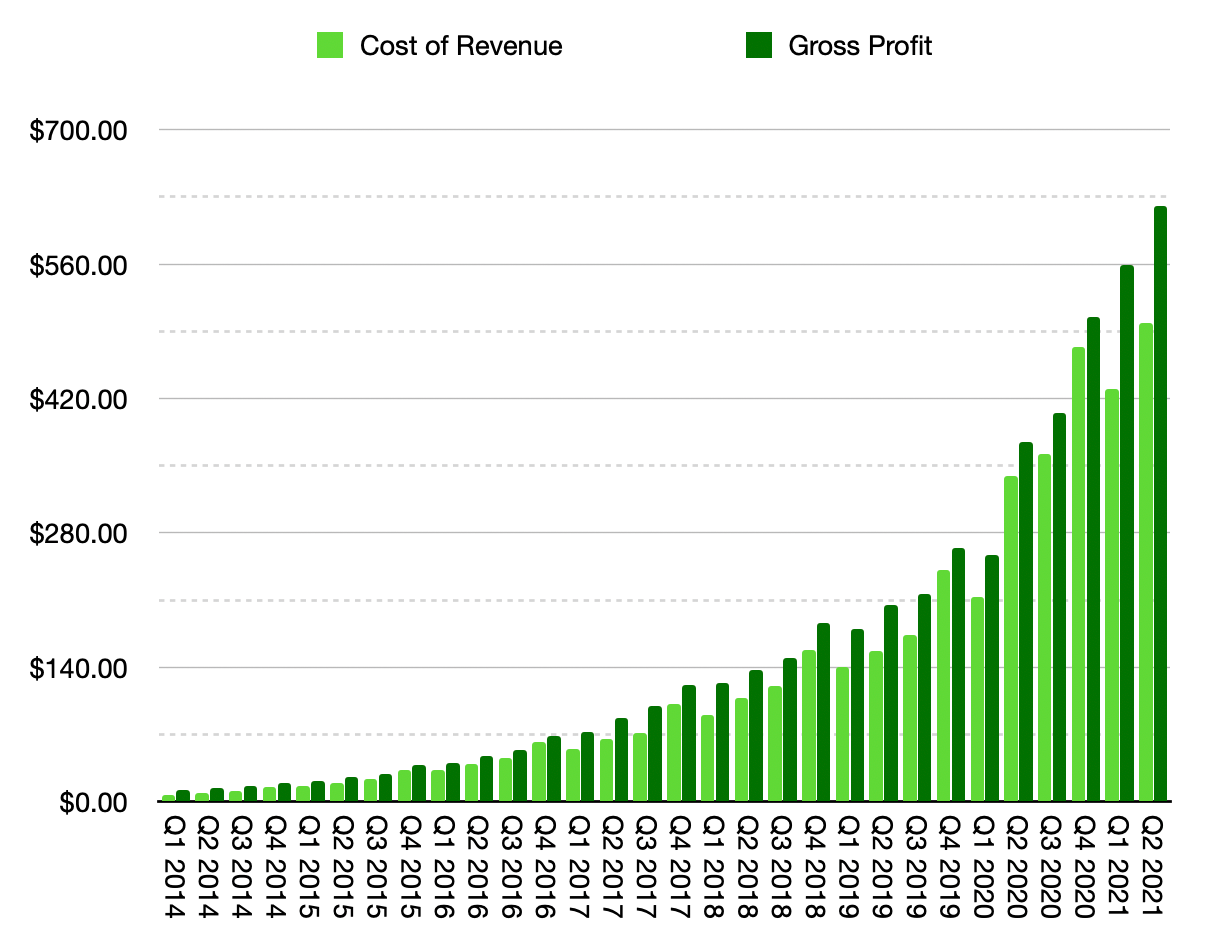

Shopify’s gross profit margin has hovered right around 55% for the better part of the last decade, but if I had to guess, I’d say that we will see this rise over the coming years as a reflection of Shopify’s merchant solutions outpacing their subscription solutions — data and software are notoriously high margin businesses. Again, this draws a comparison to Roku’s margins increasing as their platform revenue dwarfs their hardware revenue.

While both are sparatic and vary greatly quarter to quarter, Shopify’s average quarterly increase in cost of revenue is slightly greater than their average quarterly increase in gross profit, coming it at 17.16% and 15.13%, respectively, over the past 6.5 years. This statistic isn’t necessarily apparent when viewing the graph of the two, though. Rather, I think it is easier to notice that Shopify’s gross profit has yet to be lesser than the company’s cost of revenue.

Shopify’s operating expenses over the years, as expected, have been… large. That said, Shopify recently passed a pretty exciting milestone — in 2020, they reported total operating expenses of $2.84B, but posted full-year revenue of $2.93B, marking the first profitable year in company history. Below, you will see three graphs:

a graph of Shopify’s operating expenses by quarter since 2014

a graph comparing Shopify’s yearly operating expenses and revenue

a graph showing Shopify’s operating expenses composition in 2020

I’m no fortune teller, but I can confidently say that I’m betting on Tobi Lütke to continue this trend of profitability.

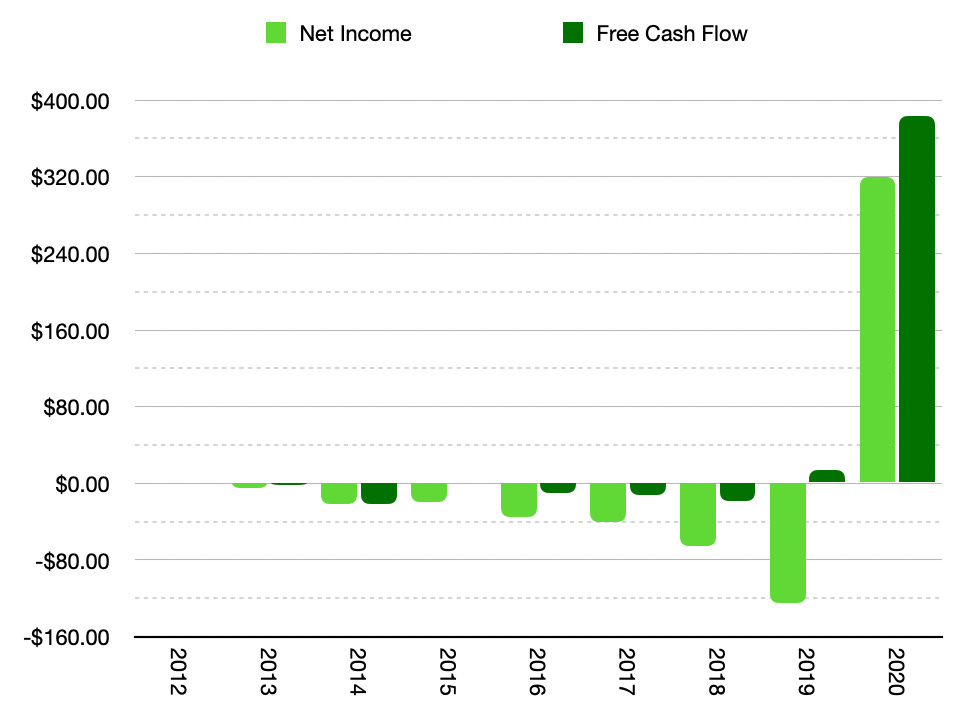

Let’s move on to Shopify’s net income and free cash flow. See if you can tell whether the pandemic gave Shopify a boost or not.

Could you tell? Jokes aside, 2020 was a gargantuan year for Shopify, with the company increasing net income by $445M and growing free cash flow by an enormous 2,665% — keep in mind, this growth is occurring in a company that has been around for fifteen years.

Shopify’s balance sheet looks incredibly healthy. Currently, the company is sitting on:

$8.46B in current assets

$11.96B in total assets

$511M in current liabilities

$1.84B in total liabilities

Thus, the company’s assets are able to pay off their liabilities over sixfold, thus leaving plenty of cash for Shopify to explore with investments and acquisitions, should they choose.

Now comes the fun part. As I have always felt that financials only tell part of the story, let’s look at some of Shopify’s useful operating metrics. Namely, we will be examining Shopify’s:

Gross Merchandise Volume

$42.2B in Q2 2021, up 40% year-over-year

Gross Payments Volume

$20.3B in Q2 2021, up 51% year-over-year

Monthly Recurring Revenue

$95.1M in Q2 2021, up 67% year-over-year

Revenue & Merchants by Region

NA density is mainly United States and Canada

LATAM density is mainly Brazil, Colombia, and Chile

APAC density is mainly Australia, New Zealand, and India

EMEA density is mainly Western Europe

Now, let’s glance at Shopify’s stock price, past year, market cap, institutional ownership, and short interest:

Shopify currently trades at $1,355.78 and is up 19.77% over the past year.

Shopify has a market cap of $170.25B with 113.22M shares outstanding.

1.62M shares are currently being shorted, giving Shopify a short interest percentage of 1.42%.

Shopify has an institutional ownership of 67.10%.

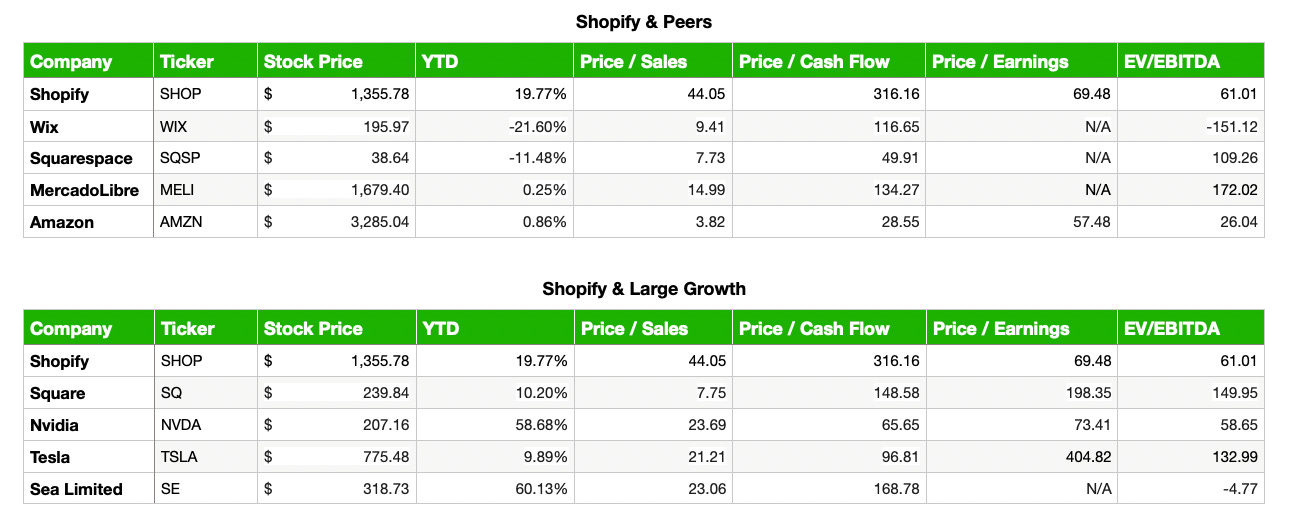

Lastly, let’s compare Shopify not only to some of its “peers” within the eCommerce platform realm, but to fellow “large growth” companies as well, from a valuation standpoint.

I would keep in mind that all of the above companies are at very different points in both their lives — publically traded and privately owned. With that said, I’ll let you decide how well valued Shopify is.

Thus, our article has come to an end.

I truly hope you enjoyed reading this article as much as I enjoyed writing it. Shopify is a staple in many portfolios and a huge compunder in many more. Excellent management, execution, and vision has propelled Shopify to where the company stands today, and will undoubtedly push them to new heights in the future.

If you’d like to receive updates each time a future issue of “Five Minute Financials” or “Business Breakdowns” is released, please consider subscribing by clicking the button below.

Thanks for reading! I wish you all nothing but the best.

— N