CrowdStrike — Q1 2022

A quick breakdown and update of CrowdStrike's most recent financial statements, stock price, valuation, and short interest.

CrowdStrike became a publicly traded company during the summer of 2019 and traded relatively sideways until hitting the March lows in 2020. Since then, they have exploded onto the scene, taking the cybersecurity space by storm… with the stock price to show for it.

CrowdStrike may have revolutionized the future of cybersecurity forever in June of 2013 when they deployed their visionary product, known as “Falcon” — a single-agent, cloud-native endpoint and workload protection software powered by artificial intelligence that detects and prevents enterprises from cloud-based threats, such as attacks on AWS, Azure, Google Cloud, and iCloud.

Man, that last sentence sure was a mouthful. Good news — we are done with CrowdStrike’s background and can officially begin reviewing the company’s financials. No more cybersecurity gibberish!

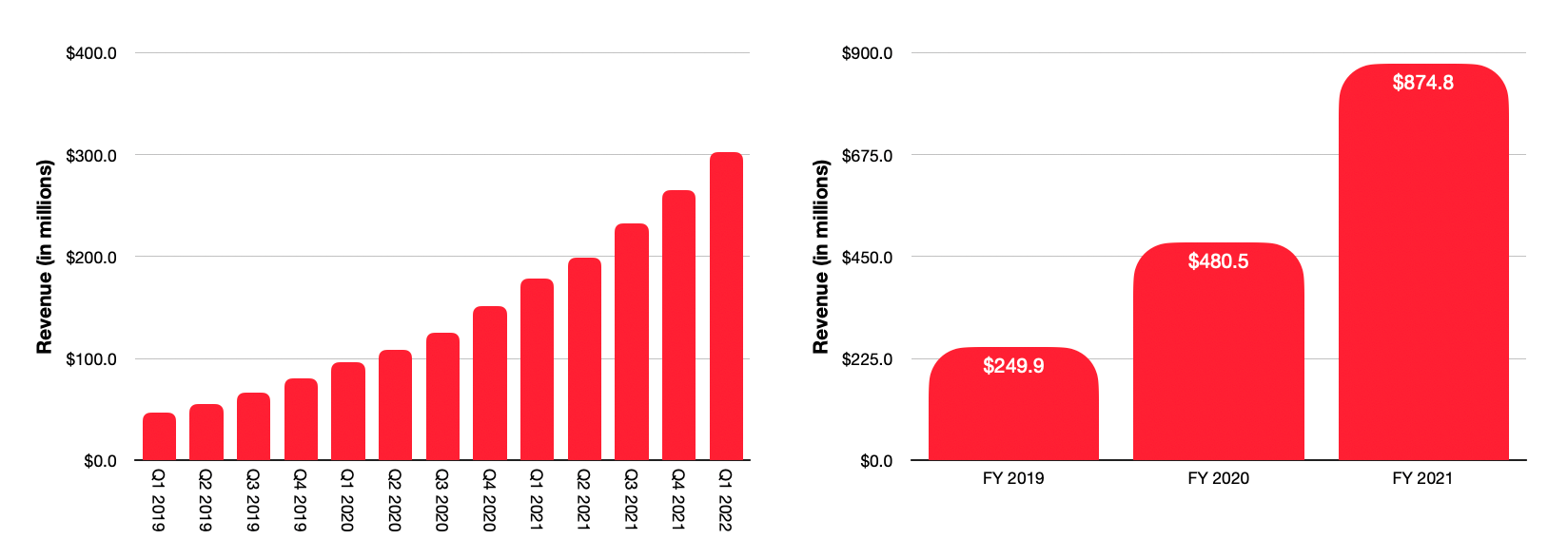

First and foremost, let’s clear something up right away: CrowdStrike operates a year ahead. Last year was their fiscal year of 2021, and their most recent quarter was Q1 2022. Alright, now that there should be no more confusion, let’s begin.

In 2021, CrowdStrike posted a total revenue of $874.8M — a growth of 82.1% year-over-year from 2020’s total of $480.5M. Then, in Q1 2022, CrowdStrike announced that they did $302.8M in the first quarter, which was a little over a 70% increase year-over-year and beat guidance by about 5%. Just for reference, CrowdStrike’s Q1 2022 revenue was 21.1% more than their full-year revenue in 2019 — pretty incredible growth. At this rate, the company should do well over $1B in full-year revenue for the first time in history.

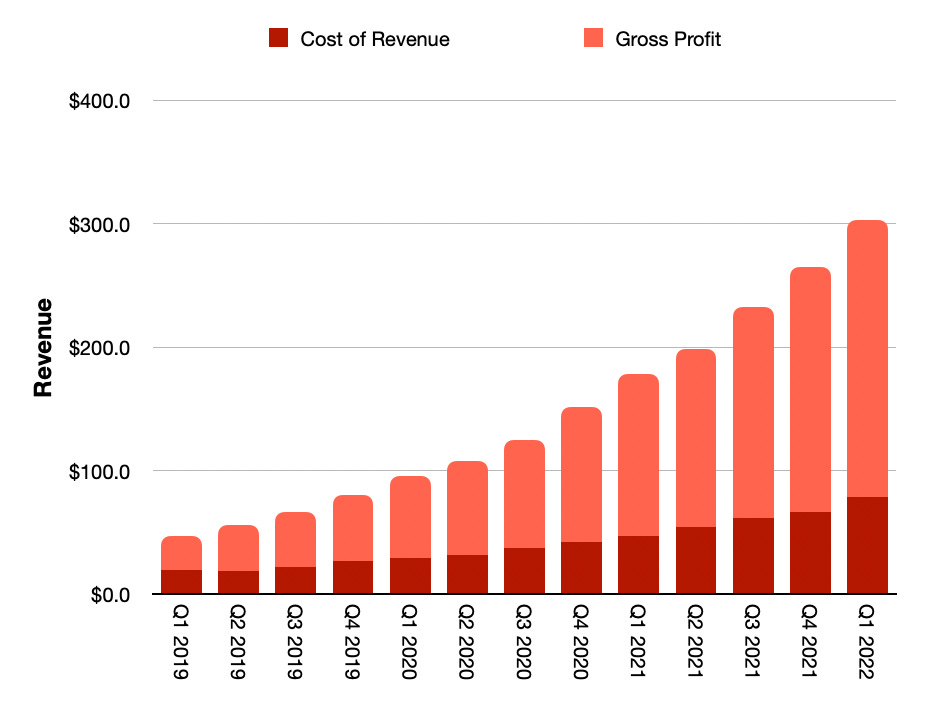

Obviously, with the growth in revenue comes growth in cost of revenue and growth in profits. Over the last 13 quarters, CrowdStrike’s cost of revenue has been growing at an average of 12.56% quarter-over-quarter, with the company racking up revenue costs of $229.9M in 2021 and $78.5M in their most recent quarter.

Over that same time frame, gross profits have been increasing at an average of 19.11% quarter-over-quarter — this might not seem like a huge difference, but it compounds very nicely as years go on, as you’ll see in the chart below. In 2021, the company posted gross profits of $644.9M, an 89.8% increase from the year prior. CrowdStrike continues their climb in 2022, announcing gross profits of $224.3M in the first quarter — again, at their current pace, the company will likely surpass $1B in gross profits for the fiscal year.

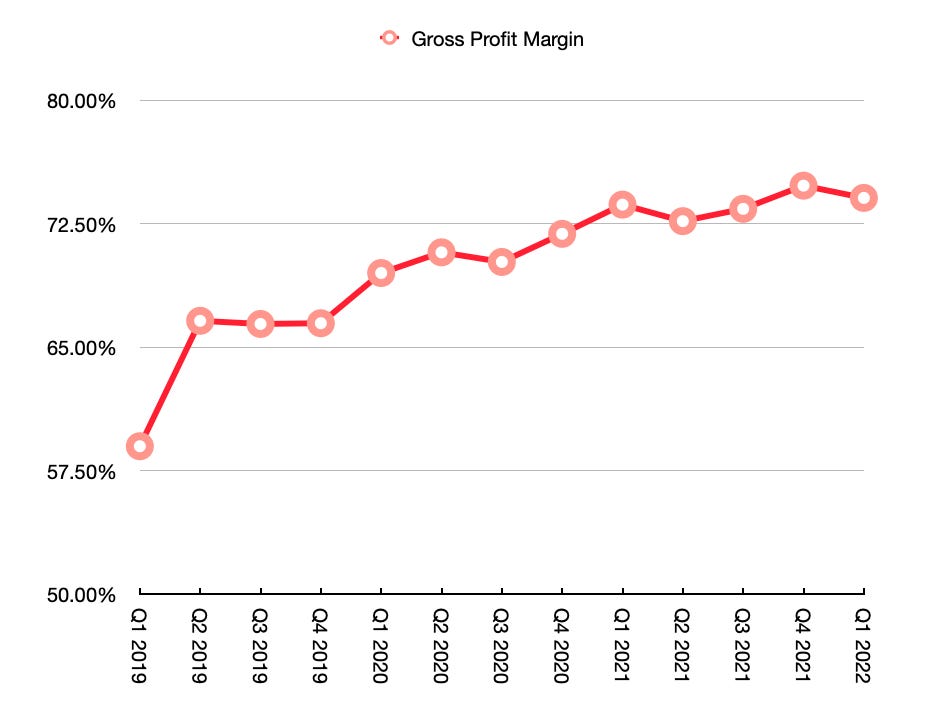

Importantly, CrowdStrike’s gross profit margin percentage has been on the rise as well — it has increased 1509bps from Q1 2019 to Q1 2022, most recently reaching 74.08%. In general, software-as-a-service business models are able to squeeze out pretty impressive margins, and CrowdStrike is no different. I imagine over the coming years their margins will continue the slow climb, likely plateauing around 80% range.

Naturally, as is the case with all growing companies, CrowdStrike’s operating expenses have been growing as well. In 2021, CrowdStrike racked up $737.5M in operating expenses, up from $485.9M in 2020. This is typical for early companies that bet on themselves, and revenue is growing significantly faster than operating expenses, so there really isn’t much to see here. Below you will see a graph of CrowdStrike’s operating expenses over the last 13 quarters, as well as its composition.

And, just because I thought it would be neat, I went ahead and created the following graph — it outlines CrowdStrike’s growth in revenue, profits, cost of revenue, and operating expenses over the past 13 quarters, and lays them all side-by-side.

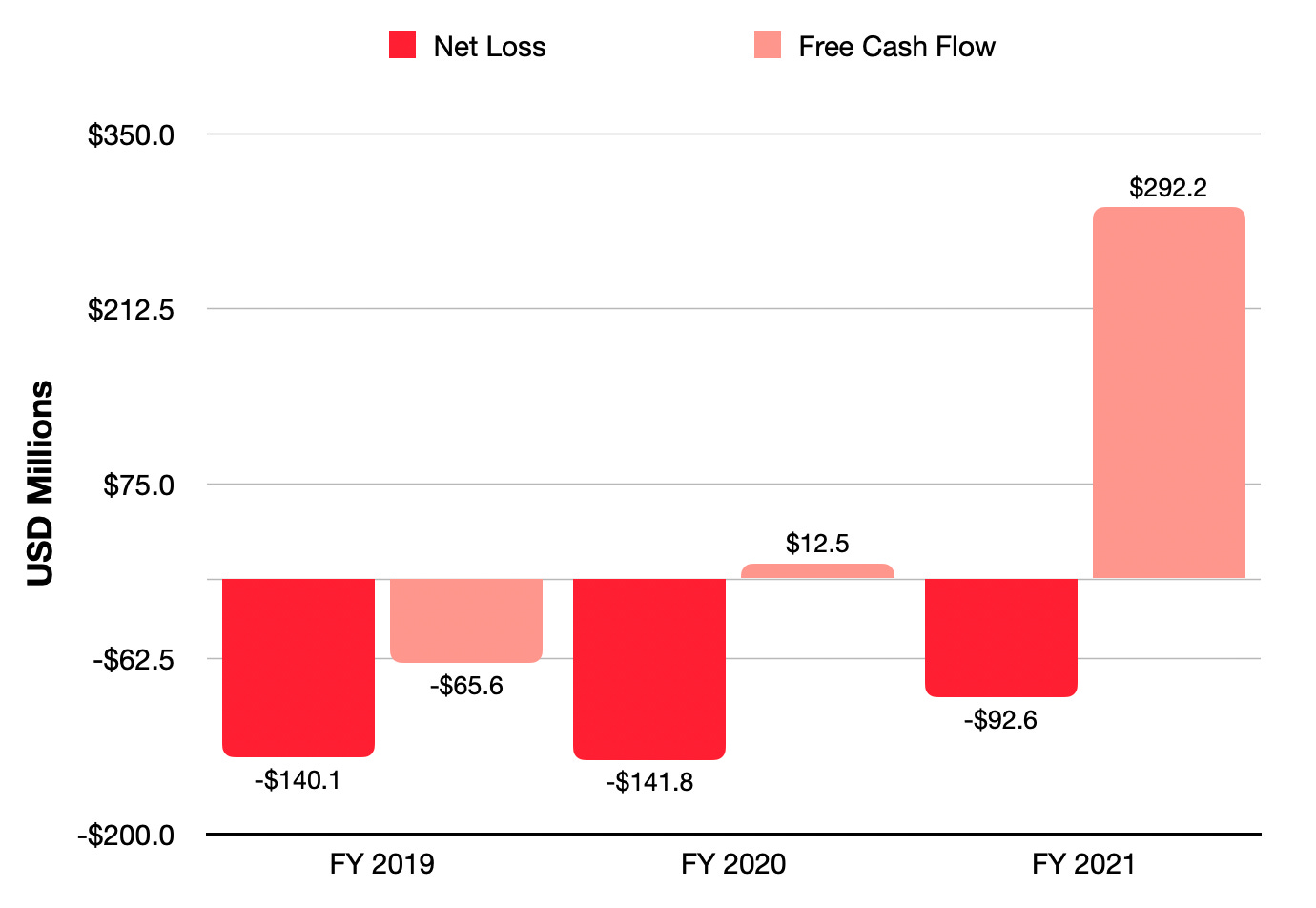

After adding in the extra expenses, CrowdStrike posted a net loss of $92.6M in 2021, but they are trending in the right direction — the company shaved off about $50M in losses from the previous year.

On the other hand, CrowdStrike’s free cash flow has shown enormous improvements — in 2021, the company announced that they had $292.2M available in cash, a 2,237.6% increase year-over-year.

Thus, while not yet profitable, the tools are certainly there. If I had to make a guess, I’d say achieving profitability is still a few years away.

As of Q1 2022, CrowdStrike is currently sitting on:

$2.04B in current assets

$2.88B in total assets

$982.77M in current liabilities

$2.03B in total liabilities

That gives CrowdStrike an assets-to-liabilities ratio of 1.42, which is respectable.

Finally, let’s look at some useful operating metrics that help guide CrowdStrike’s growth and efficiency. We will be looking at:

subscribing customers

annual recurring revenue

CrowdStrike’s subscribing customers have increased quarter-over-quarter at least since the company became public, with them gaining 1,524 new subscribers in Q1 2022 (compared to the 1,480 in Q4 2021). Likewise, CrowdStrike’s annual recurring revenue has also shown steady growth in the right direction, as seen in the chart below. In Q1 2022, the company announced that ARR increased 74% year-over-year and grew to $1.19B — of this $1.19B, $143.8M was new ARR added during the quarter.

Personally, I don’t see either of these metrics faltering for quite some time. We are still in the very early innings of cybersecurity, and the game hasn’t even started yet with cloud computing — CrowdStrike blends these two together in the most beautiful way possible, and will serve as a dominant end-point protection for cloud-based attacks for many years to come.

Lastly, let’s take a peek at CrowdStrike’s current stock price, valuation, and short interest (as of July 22nd, 2021, the time of this article’s writing):

CrowdStrike currently trades at $263.04 and is up 153.63% over the past year, via Yahoo Finance.

CrowdStrike has a market cap of $59.36B with 225,810,000 shares outstanding, via Yahoo Finance.

9,530,000 shares are currently being shorted, giving CrowdStrike a short interest percentage of 4.22%, via MarketBeat.

CrowdStrike has a forward P/E of 666.67and a P/S of 55.96, via Morningstar.

CrowdStrike has an institutional ownership of 69.93%, via Nasdaq.

Now, let’s compare these numbers to that of CrowdStrike’s peers — namely, other cloud computing and cybersecurity companies.

Palo Alto (NYSE: PANW) has a forward P/E of 45.06 and a P/S of 9.44.

Oracle (NYSE: ORCL) has a forward P/E of 19.49 and a P/S of 6.70.

Zscaler (NASDAQ: ZS) has a forward P/E of 434.78 and a P/S of 51.49.

SentinelOne (NYSE: S) has a forward P/E of N/A and a P/S of 84.61.

Fortinet (NASDAQ: FTNT) has a forward P/E of 70.92 and a P/S of 16.09.

Again, these companies are all at very different stages of maturity, with CrowdStrike being most closely related to Zscaler and SentinelOne in terms of growth and age. Ultimately, if you want to invest in the cloud computing and/or cybersecurity space, who you choose to invest in will come down to what type of an investor you are.

And there we have it — another issue of “Five Minute Financials” in the books.

I truly hope you enjoyed this issue of "Five Minute Financials" — if you did, please consider subscribing for future financial updates and reviews. If you want to check out my other “Five Minute Financials” click here. If you want to dig deeper into companies, feel free to visit my “Business Breakdowns” page here.

Like always, it’s been a pleasure. Until next time!

— Nick